According to the U.S. Department of Agriculture, the family farm is going strong. Some 98% of the nation’s farms are family farms, and these operations are responsible for 88% of the production. Here are a few things to consider for Farm Succession Planning.

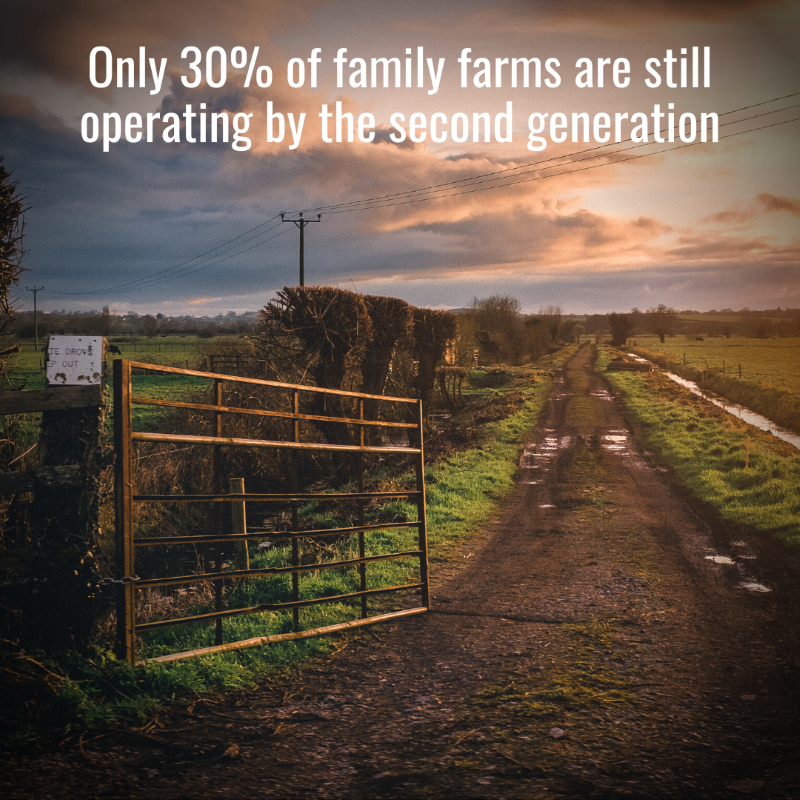

However, things may be far less rosy if you’re a farmer who is hoping to pass your farming operation on to the next generation. As Open Advisors notes, the statistics are sobering. Only 30% of family farms are still operating by the second generation. A mere 12% survive into the third generation.

While nearly 70% of family farm operators expect their operation to continue as a family business after they’re gone, only 23% have created a formal succession plan. That’s especially worrisome when the average age of the American farmer is now 57.5 years. It increased yet again with the USDA’s 2017 Census of Agriculture.

Although establishing a succession plan may be an uncomfortable task, having an effective plan is one of the best things you can do to pave the way for your farm’s future success.

What Is Farm Succession Planning?

Succession planning is about figuring out how to pass the baton to the next generation. As Investopedia explains, it involves creating a plan for the smooth transfer of the leadership, and in many cases, the ownership, of a company or business so that when the current owners leave, retire, or pass away, the company can continue to thrive.

Effective succession plans generally involve training opportunities for rising managers so that they can hone their skills and develop a thorough understanding of the company. They also tend to contain financial plans that address the current and future financial needs of all involved parties.

Farm Succession Planning Versus Estate Planning

What about estate planning? Succession planning is vital for business owners. Estate planning is essential for everyone. As NerdWallet explains, estate planning is the process of deciding who will handle or inherit your various assets if you’re incapacitated or you pass away. It generally involves things like wills, medical care directives, and retirement plans.

Business ownership, land, and other assets that are critical to your agricultural operation’s success are likely to be part of your estate. That means that elements of estate planning should be a part of your farm succession plan. But traditional estate planning won’t be enough for farm owners.

Succession planning requires thinking about a bigger picture, so there are more things that you’ll need to consider.

Things to Consider When Creating Your Farm Succession Plan

Farming isn’t an easy business. There’s much more to it than most people realize. The same is true of farm succession planning. With the huge variations in operation size and circumstance, trying to put any type of cookie-cutter solution in place would be foolish.

The differences in state laws and the potential for changes in both the federal and state laws that impact businesses, financial instruments, and inheritance matters mean that it’s best to find a team of professionals who you can trust to work with you to help you shape and maintain your customized succession plan. What types of things do you need to consider?

Your Retirement

When you pass the farm to the next generation, you’re giving up a source of income. In some cases, you may also choose to hand over the homestead. You’ll need to have a plan to replace those things. Investing in stocks, bonds, and other investment vehicles is one way to create a retirement portfolio.

Your plan may also call for you to retain the income from assets like:

- cell towers

- billboards

- natural gas

- rental properties

- and more

So that you can support yourself during your retirement.

You may also want to be sure that you have proper coverage for long-term care. If you don’t, you run the risk that nursing homes or other care facilities could end up with key chunks of the agricultural business that you worked hard to build and intended to pass to your heirs.

Your Heirs

Do you have a successor who’s capable of taking on the task of running the farm? Do they want the job? Don’t assume. Communicate.

Talk with your planned successor and make sure that they’re on the same page. If they aren’t yet actively involved in the farm’s operations, be sure to check periodically that they’re still interested in taking over at some point in the future. After all, circumstances, and plans, can change.

What if you have more than one potential successor who wants to take an active role in the operation? That can create an even trickier situation.

Can they share responsibilities and work together? If not, can you separate the operation in a way that allows them to operate independently and still provide the opportunity for a viable agribusiness?

What about any nonfarming heirs?

How can you acknowledge them while still ensuring that the business that you’re leaving to your farming heirs still has the resources that it needs to function successfully?

Are there nonfarming assets like life insurance that you could use for them?

Be prepared for hard feelings. It’s not uncommon for nonfarming heirs to feel like they’re being treated unfairly or receiving less. After all, the land, equipment, livestock, and other assets needed for even a small agricultural operation typically have a high cash value, and many business-savvy farmers also try to leave their farming heirs enough cash to help with inheritance taxes. Again, clear communication may help.

The Management Transition

No one is born knowing how to run a business. Even those who grow up working in a family business that they love and plan to eventually helm can have dangerous blind spots if they don’t actively train for the position that they will eventually hold.

Once you’ve identified your successor or successors, it’s time to talk with them and begin creating a plan for how management of the business will eventually transition to them. As Iowa State University indicates, you’ll need to consider elements of both power distribution and training:

- Decision-making should be collaborative. While there may be limits, always deferring to senior members for all decisions should be avoided.

- Developing management skills in the incoming generation should be a priority.

- Encourage cross-training to hone skills and gain experience.

- Normalize routine communications that keep everyone in the loop.

- Schedule regular, non-threatening evaluations to provide team members with useful feedback.

As your successors provide management input and labor while they learn the business, you’ll also need to address the issue of compensation. Cash is one way to compensate someone for their time and efforts. In this situation, compensation could also come in the form of equity in the business.

Minimizing Tax Burdens

Farmers are more than twice as likely to receive a bill for federal estate taxes than nonfarmers, according to MyFarmLife.com. It can be a devastating blow at a delicate time. Using gifting, trusts, and other tools to help minimize the tax burdens on your business can help facilitate a successful transfer.

Did you know a farmer is twice as likely to commit suicide than a war veteran? Get help now. Here are 8 free farmer suicide hotlines & resources.

Working with a team of financial professionals who understand your goals and concerns can help you establish an effective plan. Once established, even the best plans will need to be reviewed and updated periodically.

Life’s Uncertainties

“Life is what happens while you are busy making other plans.” John Lennon is just one of many people who gets credit for that statement. No matter how carefully you plan, you cannot plan for everything. Families grow through marriages and births. Unexpected illnesses and deaths occur. Divorces happen.

Make it a point to review your succession plan periodically. If something that demands action occurs between reviews, make an appointment with the appropriate professional to go in and make the necessary adjustments.

Having a plan that’s up to date protects you, your heirs, and your business.

Putting Together Your Plan

Farm succession planning is an intimidating task. It’s complex and emotional. However, it’s also something that you can do to help set the stage for your business’s future success. Fortunately, you don’t have to do it alone. In fact, the High Plains Journal reports that there are three areas where professional guidance can be critical to the creation of an effective farm succession plan:

- Identifying the financial needs of current and future generations.

- Ensuring a smooth financial transition.

- Balancing the needs and expectations of both farming and nonfarming heirs.

When you reach out to an experienced farm succession planner in your state for advice, that professional could be an attorney, insurance agent, financial planner, certified personal accountant, or some other experienced business professional. However, you may find that you need a team of professionals to get the best results. How do you decide who to work with? As you fill each slot on your team, look for a reliable expert with a solid reputation. Choose someone you like and respect that you’re comfortable working with. Be sure that they’re familiar with the challenges of estate and succession planning for agriculture.